The US president just announced a 5-day halt to strikes on Iran’s energy infrastructure. This most likely signals that Washington recognizes what further escalation of this conflict would cost. Everything now depends on the US finding a solution in just a few weeks – one that almost certainly means leaving the Iranian regime intact, despite regime change having been an explicit American objective from the start. It is urgent because the global economic pain is already materializing in at least three distinct but interconnected layers.

1. Energy, inflation and debt

Higher energy prices feed directly into inflation expectations – and therefore into the interest rates set by central banks and demanded by fixed-income investors. Recently, these higher interest rates have already exposed deep liquidity stress in private markets, which threatens to spill over into institutions who hold these assets – like pension funds. This alone could be a sufficient reason for the US to find a way to stop the conflict.

2. The AI boom's hidden supply chain

Less visible but equally significant is the threat to the inputs that power the artificial intelligence boom. Data centers and the computer chips that run them depend not only on cheap energy, but also on a set of industrial chemicals (like helium, sulphur and bromine) that are mainly sourced from the Middle East and are now caught in a disrupted supply chain. Since it was the AI boom that drove the majority of US stock market growth over the past three years, a sustained conflict puts that growth engine under direct threat.

3. The wealth effect and the American economy

The third layer is the large share of US consumer spending – the largest single driver of the US economy – that comes from high-income Americans, whose consumption is tied to the value of their investment portfolios. A sustained stock market decline, amplified by Gulf sovereign wealth funds pulling capital from US markets, could trigger a meaningful pullback in that spending, which could throw the American economy into a vicious downward spiral.

A narrow window for diplomacy

The current situation is straightforward: three simultaneous shocks – to energy prices, to critical technology supply chains, and to the wealth effect underpinning US consumption – arriving together would strain the global economy in ways that no single policy can easily offset. Without a genuine diplomatic breakthrough in the coming weeks, the world could be facing an economic crisis that rivals anything seen in a generation.

If we zoom out beyond the immediate crisis in the Strait of Hormuz, a larger pattern becomes visible that has been building for years: global capital is increasingly looking beyond the United States.

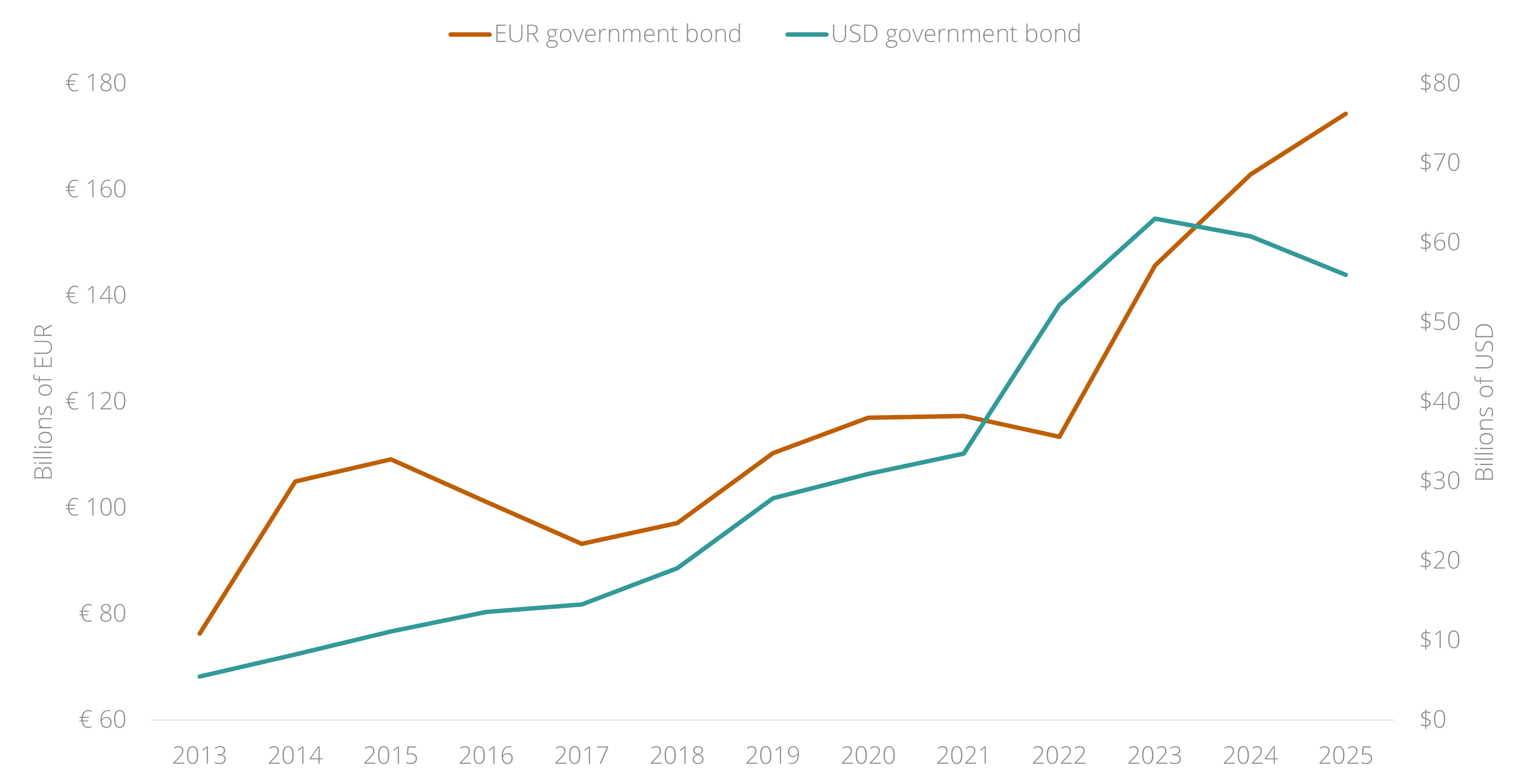

In the past few years, global investors have repeatedly confronted a question that once seemed unthinkable: whether US government bonds still deserve their status as the world's safest asset. It began in 2020–22, when pandemic-era government spending in the US pushed its budget deficit to a record high. The inflation that followed drove up interest rates and pushed down US government bond values – the assets that global investors relied on to protect their portfolios when other markets fall. In 2024–25, President Trump's attacks on central bank independence and his extreme import tariffs reinforced the same dynamic. In 2026, US military escalations against Iran, Venezuela and Greenland have brought some foreign investors to the point of considering shedding US assets altogether.

Two signals have emerged in 2026 that confirm this narrative.

The first comes from the Gulf. Against the background of Iranian officials stating that any institution buying US government bonds is financing the war, Gulf sovereign wealth funds, which hold trillions in US assets, have reportedly been in dialogue about cutting back their investment commitments to the United States, to bring capital back home.

The second comes from Europe. Since the Greenland crisis, more institutional investors are actively choosing European government bonds over American ones. This is not a rotation driven by the expectation of higher returns. It is a repricing of trust: a slow but accelerating loss of confidence in the reliability of the United States that has been building for many years.

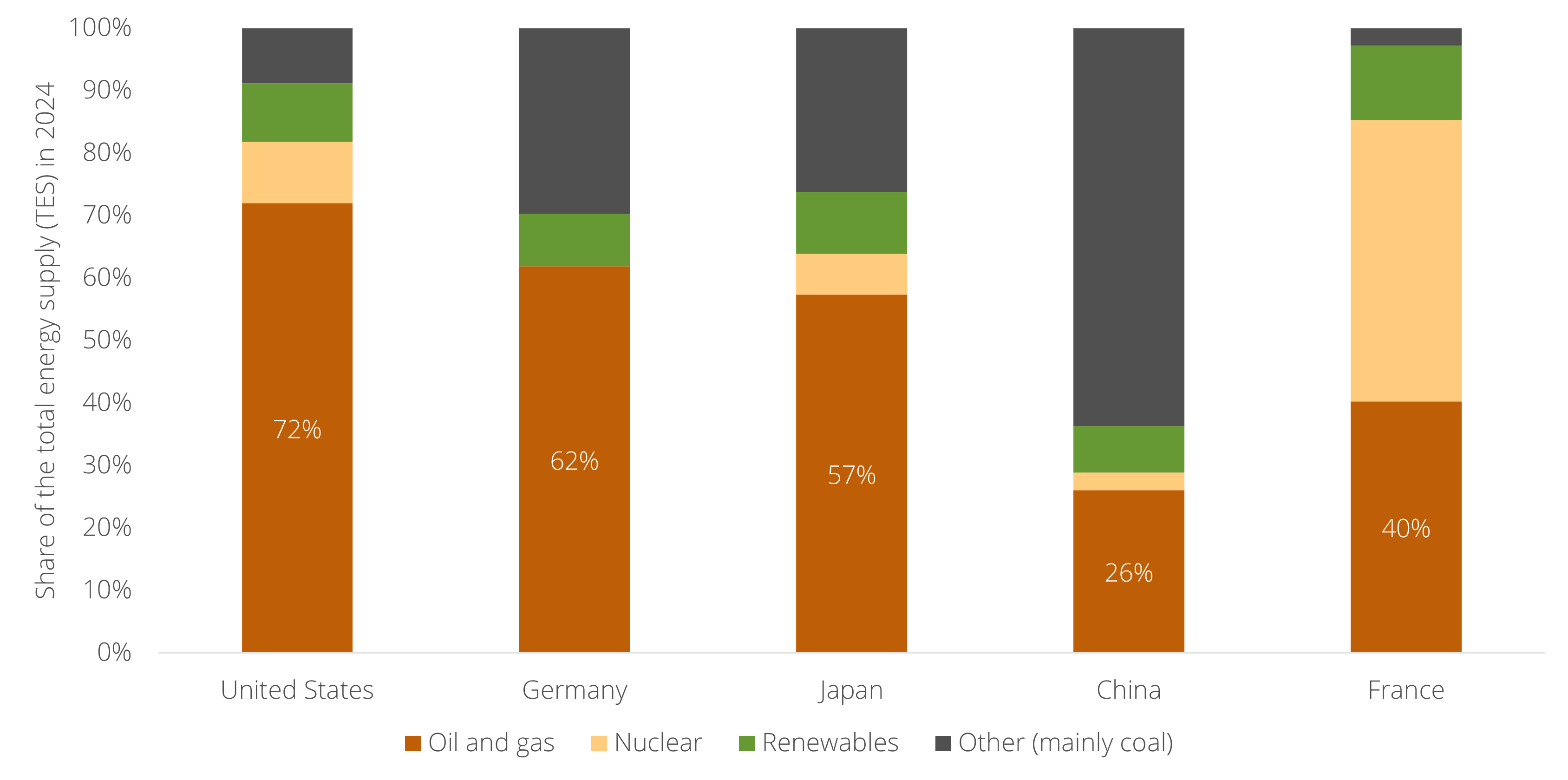

As the war in the Middle East continues to push up prices for oil and gas, two countries find themselves relatively well positioned – because they have been preparing for this scenario for decades: France and China. Both have pursued energy security through a mix centered on nuclear power and renewables, reducing their structural dependence on imported oil and gas.

For France, the vision dates to the 1973 oil crisis. Before it, France imported around 75% of its energy and had almost no domestic fossil fuel resources of its own. The response was the Messmer Plan of 1974 – a state-directed mobilization to build out nuclear capacity at a scale that remains unmatched in the Western world. Fifty years later, that bet is paying off.

In China, decades of industrial policy have been shaped by a refusal to become dependent on imported oil and gas – a vulnerability that Chinese planners call the "Malacca Dilemma": the risk that foreign powers could strangle Chinese energy supply by blocking maritime routes (like the Strait of Malacca, or currently, the Strait of Hormuz). Coal, despite its pollution, remains China's dominant energy source today, but explicitly as a bridge, not a destination. The destination is a mix of nuclear and renewables on a scale the world has never seen: more than half of all nuclear reactors currently under construction are in China, and China installs more solar capacity each year than the rest of the world combined.

The irony is that two very different political systems arrived at the same conclusion through the same logic: that the energy mix of nuclear and renewables is not merely relatively good for the environment, but offers energy security for the nation.