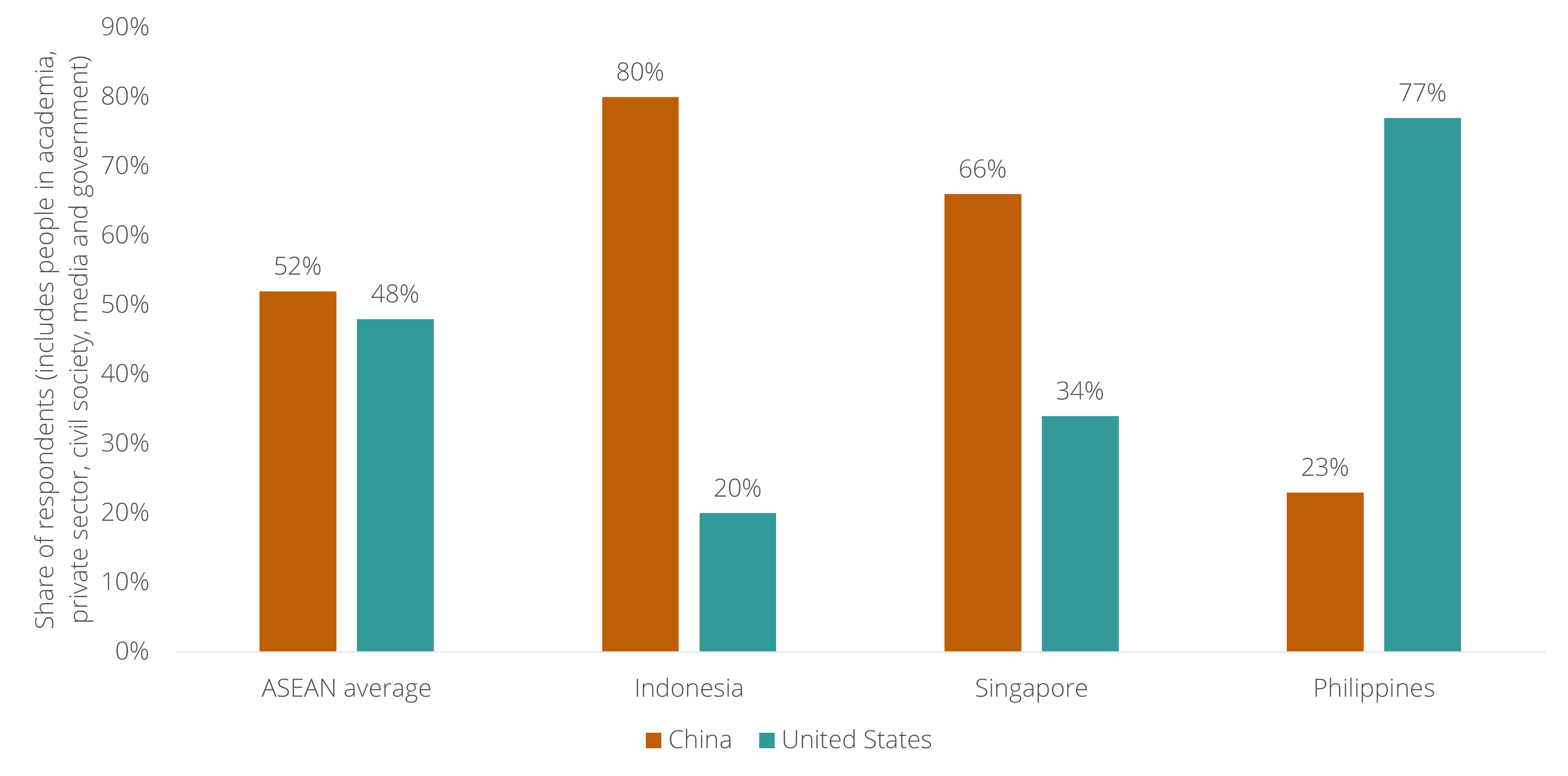

A Singaporean think-tank has found that 66% of Singaporean opinion leaders would side with China over the United States if forced to choose - a striking figure for one of Washington's closest partners in the region.

Europeans should resist filing this under "Asian story." Singapore (and ASEAN more broadly) sit in Europe's predicament: the US is their most important security partner and China is their most important trade partner – and they would rather not choose at all.

As news emerges of escalation in the trade conflict between Europe and China, it may seem naive to point to the opportunity of them working more closely together. However, we should not be surprised if that is exactly what happens in the coming years. Europe and China share a fundamental goal in the transition to clean energy, and to complete it, they need each other.

The transition to clean energy is a shared goal for Europe and China, albeit for different reasons. In China, clean energy is central to the country's economic reform plan, in which the economy transitions away from investing in real estate and infrastructure and towards high-tech manufacturing, including clean energy technologies. In Europe, besides climate targets, successive global crises have made its energy system expensive and vulnerable to disruption, necessitating a transition towards clean, local energy sources.

What is sometimes underappreciated is that, because of this shared goal, clean energy has already become a key driver of economic growth for both (see chart). In China, clean energy industries account for 25% of GDP growth; in Europe, more than 30%. In the US, the figure is just over 5%.

Most importantly, to complete the transition to clean energy, Europe and China need each other. Europe cannot achieve energy security without affordable Chinese technologies, and China cannot sustain its export model without reaching agreement with advanced economies like Europe on the rules for market access.

The key question is how exactly Europe and China will be able to cooperate amid conflict – driven mainly by Europe's concerns about overreliance on Chinese products – especially at a time when tensions are still escalating. The answer lies in the current energy crisis. Europe will increasingly discover that the greatest value from clean energy lies not in manufacturing these technologies (solar panels, wind turbines, heat pumps) but in deploying and integrating them with the local energy system, as this is what unlocks the potential of the broader economy. The Netherlands is a case in point: its congested electricity grid is already preventing new business formation even outside industrial production.

The main bottleneck for cooperation between Europe and China is therefore not economic competition but strategic security: Europe does not want to become overly reliant on a single country for its energy needs again. This will drive European policy towards a logic of diversification – as seen this week in the area of chemicals – rather than punishment (like the US approach of import tariffs on Chinese goods). This European approach could, like the Western quota policies on Japanese imports in the 1980s, provide the basis for diplomatic agreement.

Last month, Stanford University published research that contradicts the dominant narrative on US-China artificial intelligence (AI) competition. According to millions of human voters, the performance gap between the top US and top Chinese AI models has effectively closed (see chart).

Most importantly, Chinese firms are generating frontier AI capability at a fraction of the costs of US firms. According to Stanford, a 23-to-1 spending gap between US and Chinese private firms is producing a 2.7% performance gap. This has direct implications for US-based AI companies whose valuations rest on the assumption of a structural advantage. It also suggests the DeepSeek shock of January 2025 – when the launch of a single Chinese model briefly erased a trillion dollars from US tech stocks – was not an anomaly, but the first sign of a convergence that had been underway for several years and has continued since.

A key question in the coming years will be how Western investors can profit from China's AI capabilities. On April 27, the Chinese government cancelled Meta's $2 billion acquisition of Manus, a Singapore-based AI startup founded by Chinese engineers. Beijing is signaling that frontier AI capability is now treated as strategic territory in the same category as rare earths and semiconductors – and is therefore closing the offshore "Singapore-washing" route that Chinese tech firms have used for years to reach Western investors.

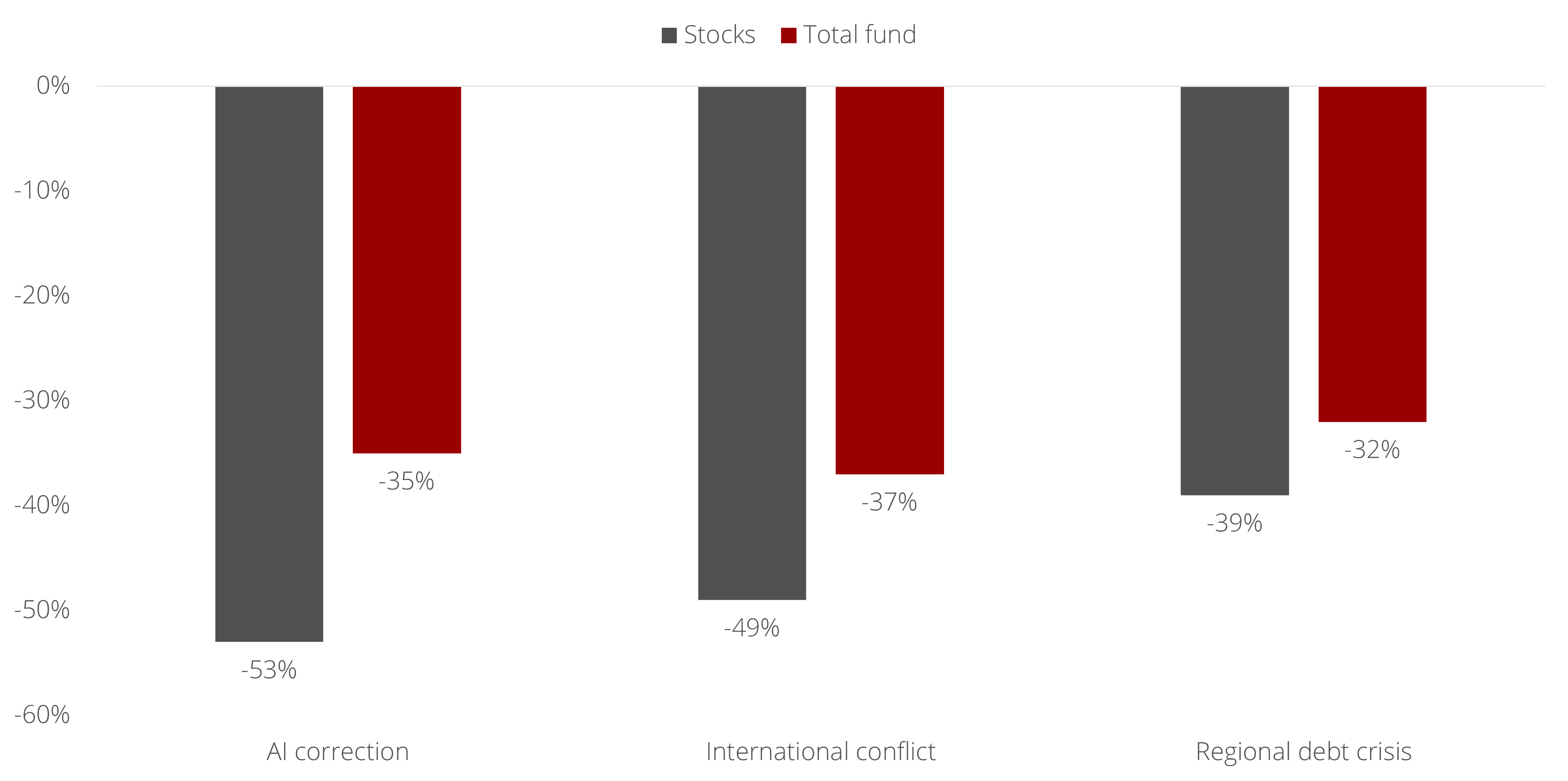

Since COVID, western societies have grown deeply dependent on government financial support during times of global crisis. The COVID response from 2020 onwards was unprecedented: the US launched the largest infrastructure investment packages in its history, while EU countries agreed for the first time to issue joint debt. The energy support packages that followed the war in Ukraine in 2022 were also significant, reaching up to 5% of GDP in some European countries. In 2026, however, as the economic impact of the war in Iran threatens to become severe, the capacity for a similar response is largely gone.

The main reason is the worsening state of government finances. Since COVID, the yields investors demand on government debt are substantially higher than six years ago. In simple terms, governments can no longer afford large-scale financial support without triggering a further rise in the yields on their debt. And rising yields, for countries already carrying high debt-to-GDP ratios, risk setting off a vicious cycle: higher borrowing costs force spending cuts, which slow growth, which worsens the debt burden, which pushes yields even higher - and so on.

A key implication is that western governments, without the ability to soften the blow of a global crisis, are losing control over the way economic pain will drive change. The early signs are already visible. In the US, the adoption of renewable energy is accelerating despite the Trump administration's efforts to protect fossil fuels, because businesses and households are discovering that renewable technology – including the Chinese-made products the administration has sought to block – offers greater price stability than oil and gas. In Europe, calls for a more stable relationship with China are growing for the same reason.

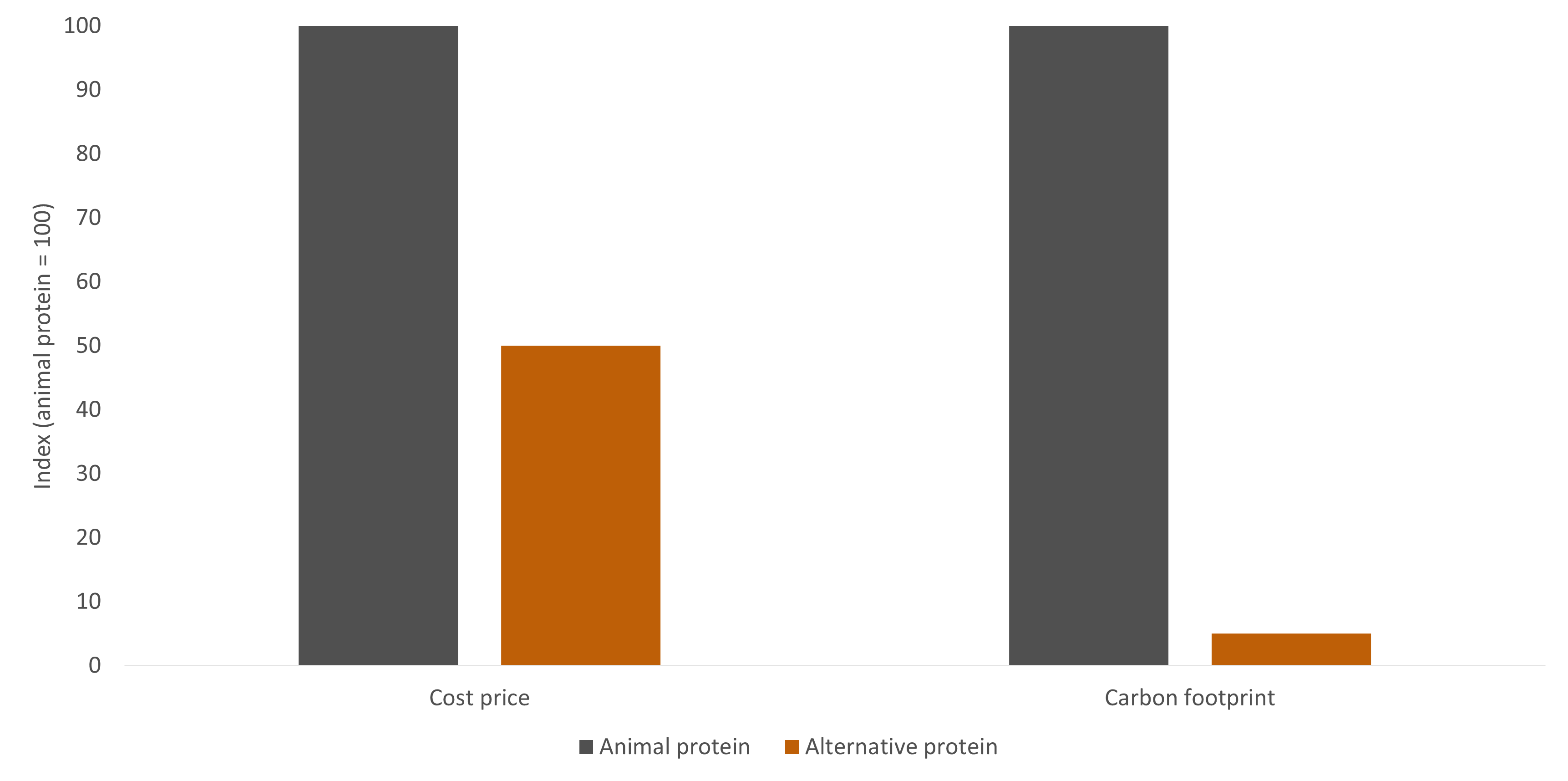

In the coming years, alternative protein (plant- and cell-based protein as a substitute for animal-based food) is likely to follow the same pattern as renewable energy technology over the past twenty years: driven by Chinese innovation, the cost falls so far that the case for transition shifts from a divisive moral ideal into a shared economic necessity.

Twenty years ago, the Chinese government made renewable energy technology a top priority for the first time in its 11th Five Year Plan (2006–2010). Today, China is the global leader in solar panels, batteries and electric vehicles. Over that period, several global crises that drove up the price of energy (the war in Ukraine, the war in the Middle East) turned renewable energy into a shared economic necessity: a more reliable energy supply at a lower cost. Something similar is now likely to happen in food, whose global prices are high and rising because of the war in the Middle East.

In its 15th Five Year Plan (2026–2030), the Chinese government has made alternative protein a top priority. China is already the world's largest funder of agricultural R&D, spending twice as much as the United States. The city of Shanghai has made the industrial scaling of alternative protein a key strategic objective. In November 2025, one Chinese company opened a factory the size of 75 football fields capable of producing alternative protein at 50% of the cost of animal-based protein - and with 95% lower carbon emissions.

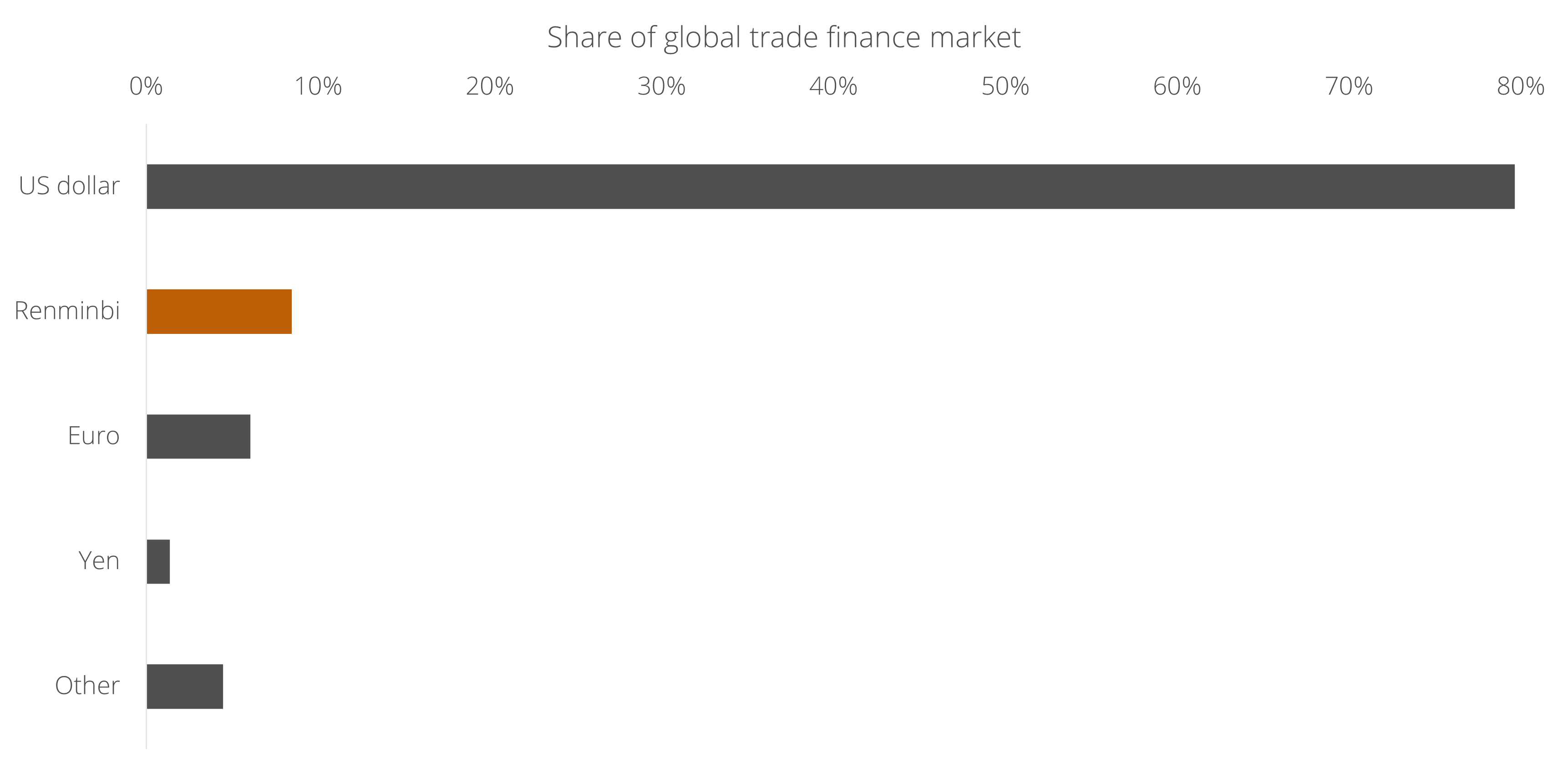

A significant signal of financial stress in the Gulf has emerged: according to the Wall Street Journal, the governor of the UAE's central bank has opened talks with the United States about a currency swap arrangement. The stability of the UAE's currency, the dirham, depends on its peg to the US dollar, which is maintained through large dollar reserves accumulated via the UAE's trade and financial networks. Those reserves are now under pressure from two directions: maritime trade disruption and capital flight – particularly in real estate, where luxury property discounts of over 50% are being reported. Together, these forces threaten a structural decline in dollar income. This is the mechanism that triggered the 1997 Asian financial crisis: when dollar reserves backing a pegged currency erode faster than they can be replenished, a currency crisis becomes self-fulfilling.

The Gulf states are therefore in urgent need of regional stability – but looking at both the US and Iran, that appears unlikely. The US is caught between three bad options: tacitly admitting defeat and watching the Iranian regime it tried to destroy consolidate into a regional power with global influence through its control of the Strait of Hormuz; muddling through while the global economy absorbs severe shocks across multiple supply chains; or risking the consequences of further military escalation. Meanwhile, according to reporting by The New Yorker, those who now govern Iran are considerably more hardline than is widely assumed – and less inclined than their predecessors to accept a diplomatic settlement favorable to the US and Israel.

All of this carries a long-term risk for the US in its rivalry with China. In their talks with Washington, UAE officials explicitly warned that the Chinese renminbi is a serious alternative to the US dollar. This warning is credible because the Gulf states have already been building the infrastructure for such a shift. The mBridge project – a digital currency platform backed by the central banks of China, Saudi Arabia and the UAE – processed $56 billion in transactions in 2025, a 2,500-fold increase from 2022. Although mBridge operates at the level of financial transactions rather than central bank reserve holdings, this is how the dollar's network effects would weaken first in a long-term shift.

As the Hormuz crisis continues, we would be wise to remember a lesson from the COVID crisis: local shortages of specific resources can cascade into larger global problems that are difficult to predict. Global attention is currently focused on energy (rising oil and gas prices), food (higher fertilizer costs) and helium (critical for computer chip production), but a closer look reveals at least three additional supply chain disruptions that could spiral into something larger.

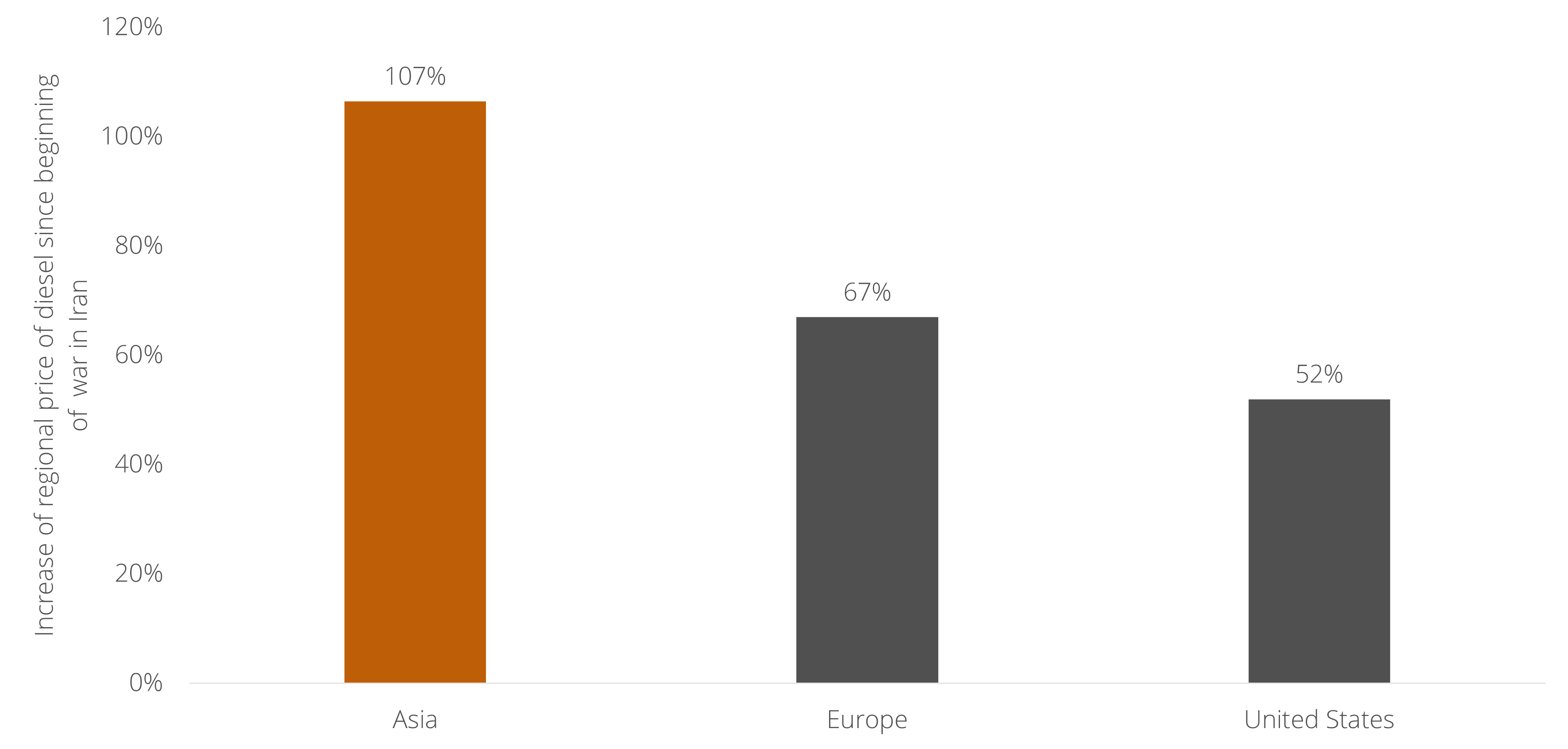

First, shortages of naphtha — refined from oil and used in the production of plastics, chips and cars — have triggered an industrial state of emergency across Asia. Both Japan and South Korea are attempting to calm markets, but supply chains are already being disrupted. In Japan, the prime minister intervened to quell online rumors of an imminent shortage after several plastic producers announced production cuts affecting sectors as diverse as food and healthcare. South Korea has banned naphtha exports to protect domestic medical procedures and has reluctantly begun sourcing the material from Russia.

Second, Australia — heavily dependent on diesel — faces rising prices and emerging shortages that threaten to shut down both farming and mining operations. As an emergency measure, several tankers carrying diesel have been sent from the US, a journey that takes up to three months, underscoring the severity of the situation. This matters globally: Australia is one of the world's largest producers of minerals like iron ore, lithium and nickel.

Third, Europe is on course to run out of kerosene within three weeks. While an aviation disruption may appear less urgent than food or mining, it would indirectly affect a wide range of businesses and economies through the collapse of tourism.

Each of these shortages may seem secondary to the broader disruption of energy, food and chip production. But together they threaten industries as diverse as healthcare, mining and tourism — and could push the global economy into territory that is difficult to predict.

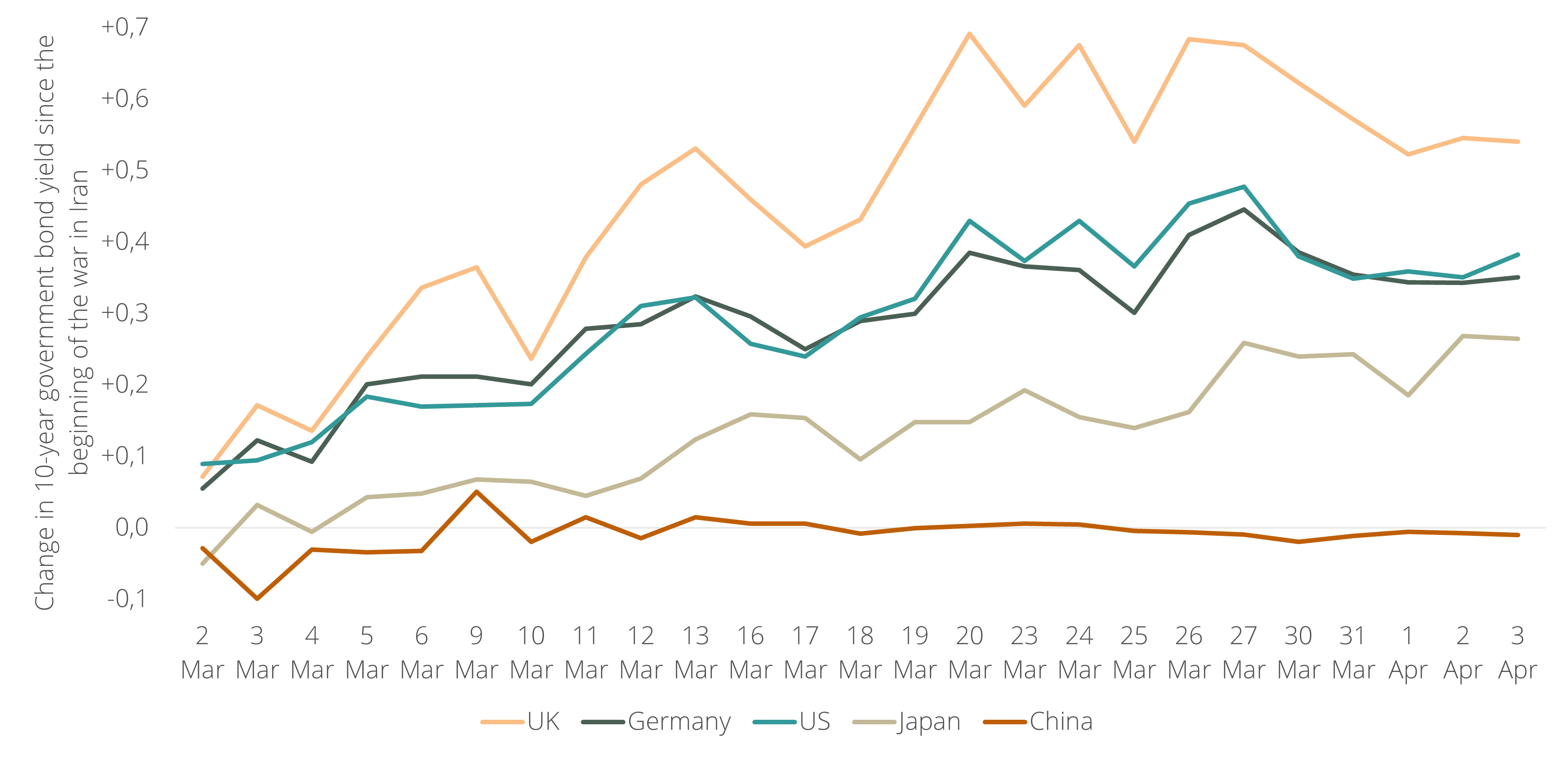

In every global crisis of our generation — the 2001 dot-com crash, the 2008 financial crisis, the 2020 COVID crisis — global investors sought safety in US Treasuries, placing capital in the 10-year US government bond. The 2026 war in Iran has broken that pattern. For the first time in a global crisis, China's government bonds are the only safe haven, holding their value while US Treasuries, other government bonds, and even gold have sold off. Meanwhile, equity markets in China have also lost less value than their counterparts in the US, Europe and Japan.

This is happening despite investors' well-documented reservations about Chinese assets — political risk, capital controls, and the difficulty of converting renminbi into dollars, euros, or yen. That is because, as we have written in the past year, China's safe haven status is part of a larger shift: trust in US stability is declining, while China is no longer seen as uninvestable, leads in technological innovation, sets global standards, has soft power and is better prepared for an era of prolonged global conflict.

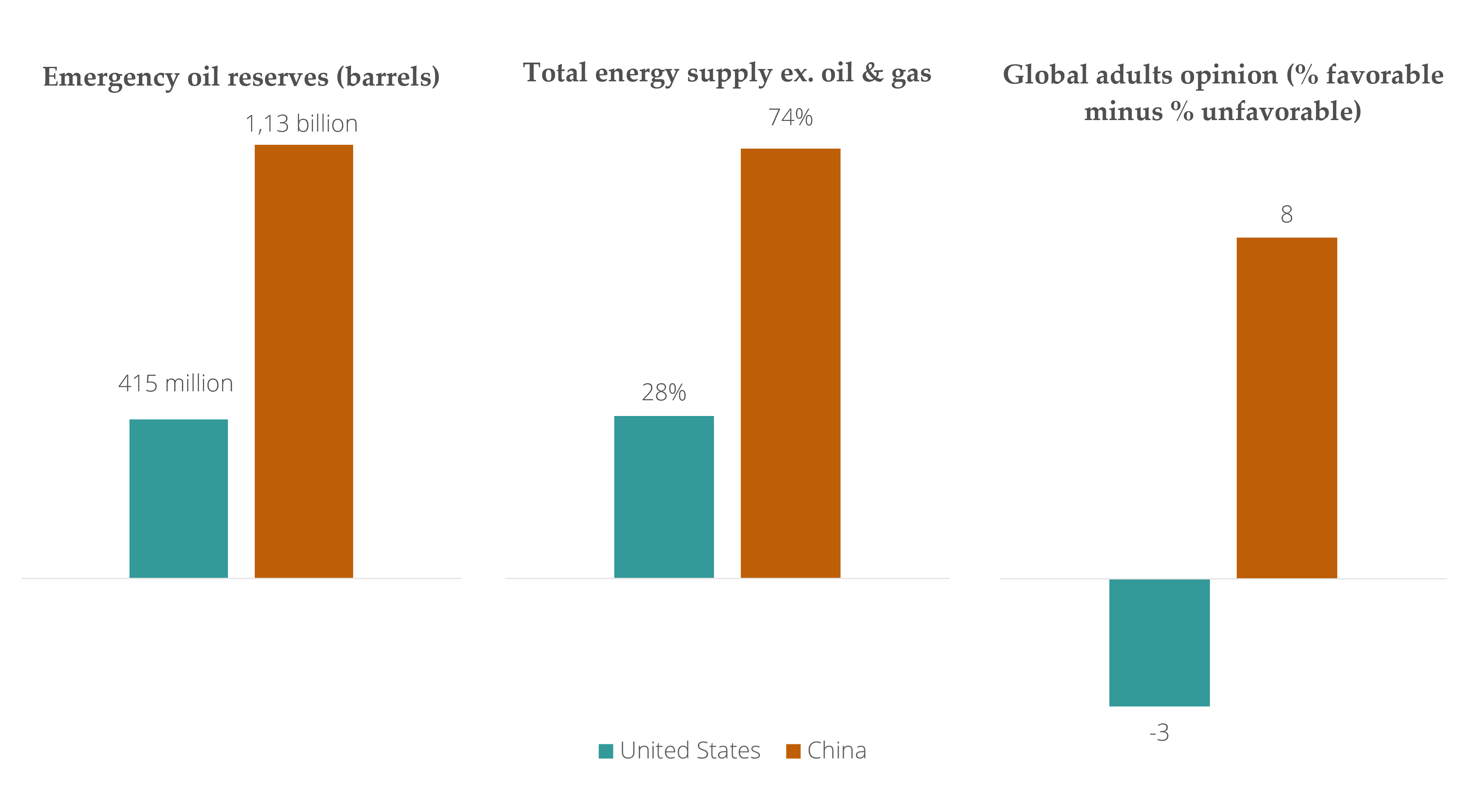

Ironically, while the US is locked in a global struggle for influence with China, it is China that was better prepared for the war in Iran — the war the US itself started. China's energy system is more resilient against a prolonged conflict in the Middle East, its businesses are the main beneficiaries of the conflict, and the conflict is improving China's reputation as a more stable international partner for trade and investment than the US.

First, China's economy is more resilient to a prolonged conflict in the Middle East than any other major economy. The main reason is the structure of its energy system. As we wrote several weeks ago, China's vision of energy security — a mix of nuclear and renewables, with coal serving as a bridge — is more resilient than the US system, in which oil and gas account for 72% of total energy supply. China also reportedly holds twice as many emergency oil reserves: 1.13 billion barrels compared to 415 million for the US.

Second, China's businesses are the leading producers of the technologies that benefit most from this conflict. In many countries, yet another international conflict driving up oil and gas prices has sparked renewed demand for renewable energy technologies such as solar panels, heat pumps, and batteries — all industries in which China is the world leader. Electric vehicles, another area of Chinese dominance, are also gaining in popularity as a result.

Third, under the second Trump administration, China is rapidly becoming a more stable and predictable international partner than the US. European leaders were already working to improve relations with Beijing before this conflict began. Global investors, meanwhile, are increasingly viewing Chinese government bonds as a relatively stable safe haven. Notably, Iran is reportedly demanding payment in Chinese renminbi from ships seeking passage through the Strait of Hormuz.

Most importantly, even if the US manages to prevent a full economic collapse in the coming weeks — as we warned last week remains a real risk — the dynamic described above is unlikely to reverse. In all three dimensions, this conflict is likely to remain a positive force for China's long-term development.

The US president just announced a 5-day halt to strikes on Iran’s energy infrastructure. This most likely signals that Washington recognizes what further escalation of this conflict would cost. Everything now depends on the US finding a solution in just a few weeks – one that almost certainly means leaving the Iranian regime intact, despite regime change having been an explicit American objective from the start. It is urgent because the global economic pain is already materializing in at least three distinct but interconnected layers.

1. Energy, inflation and debt

Higher energy prices feed directly into inflation expectations – and therefore into the interest rates set by central banks and demanded by fixed-income investors. Recently, these higher interest rates have already exposed deep liquidity stress in private markets, which threatens to spill over into institutions who hold these assets – like pension funds. This alone could be a sufficient reason for the US to find a way to stop the conflict.

2. The AI boom's hidden supply chain

Less visible but equally significant is the threat to the inputs that power the artificial intelligence boom. Data centers and the computer chips that run them depend not only on cheap energy, but also on a set of industrial chemicals (like helium, sulphur and bromine) that are mainly sourced from the Middle East and are now caught in a disrupted supply chain. Since it was the AI boom that drove the majority of US stock market growth over the past three years, a sustained conflict puts that growth engine under direct threat.

3. The wealth effect and the American economy

The third layer is the large share of US consumer spending – the largest single driver of the US economy – that comes from high-income Americans, whose consumption is tied to the value of their investment portfolios. A sustained stock market decline, amplified by Gulf sovereign wealth funds pulling capital from US markets, could trigger a meaningful pullback in that spending, which could throw the American economy into a vicious downward spiral.

A narrow window for diplomacy

The current situation is straightforward: three simultaneous shocks – to energy prices, to critical technology supply chains, and to the wealth effect underpinning US consumption – arriving together would strain the global economy in ways that no single policy can easily offset. Without a genuine diplomatic breakthrough in the coming weeks, the world could be facing an economic crisis that rivals anything seen in a generation.